THE APPRENTICE AND CENTRAL BANKS

Are CBs preparing to make mistakes?

Due to other commitments, I had to miss commenting on the volatile course of events after the Sorcerer´s Apprentice [i] struck again, unleashing the winds of war. Fortunately, the issues were not so much about the theoretical insights on what to say, and the attempts to guess what the hypermercurial Trump would do next were hopeless. Markets always followed the more optimistic path at every moment, relying on TACO and leaning towards a de-escalation of the conflict. As Trump’s domestic political difficulties worsened, the posture seems rational. Central Banks, by staying so far on hold, behaved as I predicted in my post after the beginning of the hostilities (see my post ”ECB, no hikes. FED, no cuts” here .

SUBSCRIBE FOR FREE TO GET ALL POSTS BY EMAIL

THE FOG OF WAR

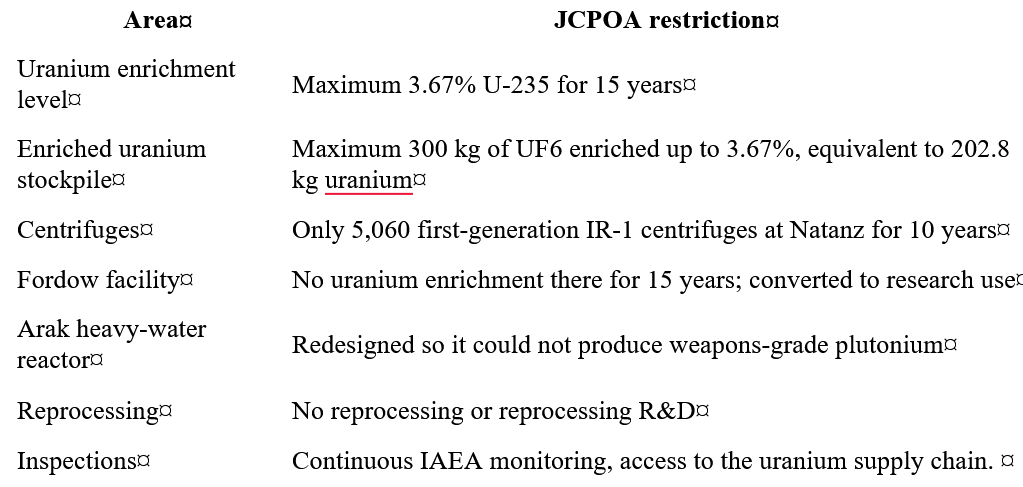

Predictably, a few weeks of bombing were not enough to engineer regime change and crush the possibility of Iran getting nuclear bombs one day. The volatile Trump embarked on a dizzy routine of big threats, false claims and predictable retreats, which have emboldened Iran´s negotiation stance. A sort of impasse seems to have been reached. This is dangerous because President Trump is hard-pressed to end the war, but some claim to declare victory regarding the opening of the Strait of Hormuz and the control of Iran´s enriched uranium. He is aware, despite being able with the help of the media, to hide it, that the progress made by Iran to enrich uranium to higher levels occurred after his 2018 decision to rip up the Obama 2015 deal with Iran to avoid that. He knows that his critics will, in the end, compare what he may achieve this time with the terms of that deal. Considering that enriching uranium to a 3 to 5% grade is sufficient for peaceful electricity production, and that, to fuel nuclear bombs, the enrichment has to reach a 90% grade, it is therefore worthwhile to recall the terms of the 2015 deal:

Iran was required to:

The monitoring agency was primarily the International Atomic Energy Agency (IAEA). Politically, implementation was supervised through the JCPOA Joint Commission, chaired/coordinated by the EU, and integrating Iran, the United States, the United Kingdom, France, Germany, Russia, and China. The UN Security Council also played a role through Resolution 2231, especially regarding the termination of sanctions. The deal worked, as the IAEA report of November 2018 stated that Iran’s enriched uranium stockpile had not exceeded the 300 kg UF6 limit and that, as of 4 November 2018, Iran held 149.4 kg of uranium enriched to 3.67% U-235, well below the Agreement´s ceiling.

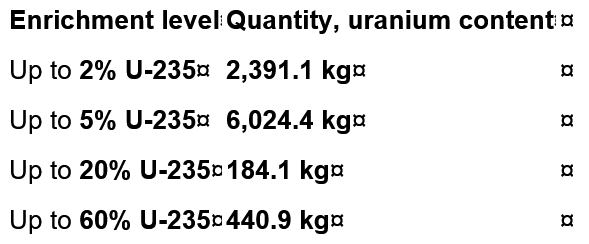

After the end of the Obama deal, Iran sped up the process of enrichment. The best public estimates are from the IAEA, with the key date being 13 June 2025, just before the time of the June US bombing of Iran sites, which, according to Trump, “obliterated” all the facilities. As of 13 June 2025, the IAEA estimated Iran’s total enriched uranium stockpile at 9,874.9 kg of uranium. Of this, 9,040.5 kg was in the form of UF6 gas, distributed as follows:

The most significant number is 440.9 kg, enriched to 60% U-235. If enriched to 90%, it could serve as fuel for about 11 nuclear bombs, according to public estimates. After the the US B2 bombings of last June, it seems that no estimate is possible about the present situation, including about the capacity of Iran to quickly continue the enrichment process. The risk now is that, to achieve short-term results, Trump may conclude that it must escalate to de-escalate and end the war. In fact, he just publicly threatened exactly that. Still, I believe/hope that some sort of settlement will happen reasonably before the November elections.

PROSPECTS FOR CENTRAL BANKS BEHAVIOUR

Policy rate decisions

The task of Central Banks is always more difficult when the economy suffers a supply shock that has simultaneous effects: upwards on inflation and downwards on economic activity and unemployment. Even for CBs, like the ECB, that have primary mandates exclusively dedicated to inflation control, the negative shock to output cannot be ignored because, indirectly, it exerts a downward impact on inflation. That is why a mandate of flexible inflation targeting for the medium term ends up being similar to a dual mandate.[i] So, whatever the mandate, central banks cannot completely ignore the significant effect that has on output deceleration and its corresponding impact on inflation.

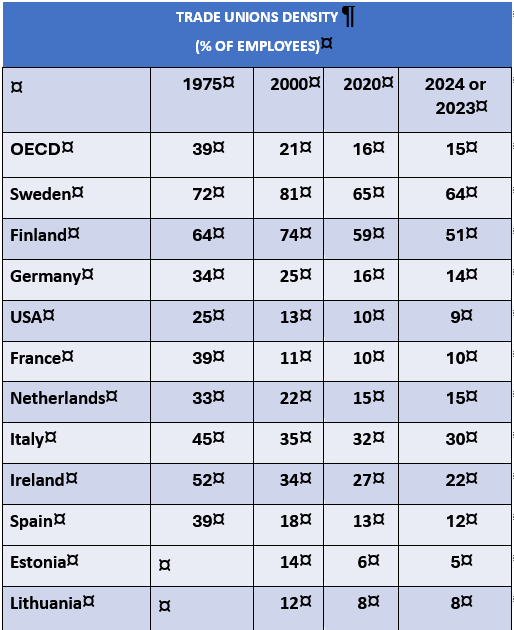

Central banks will have to calibrate monetary policy in a balanced way. They will also have to do so gradually, because wars don’t last forever, especially in this case, where one party, the US, is under strong pressure to end it soon. This implies that, for the time being, central banks should stay on hold until signs of significant second-round effects emerge. So far, none of the three possible sources of such effects has materialised: neither wages, profit margins, nor firms’ medium-term expectations. I underline the words ‘by firms’ here because, in our economies, those are the ones with a direct link to price decisions. In advanced economies, besides strong oligopolistic markets, monopolistic competition markets dominate. In such markets, with diversified products, all firms make decisions on their prices, and there isn´t a smooth market supply curve independent of demand. Those firms usually make such decisions using a cost markup method where wages are included. However, in advanced economies, workers’ power to influence their wages has been declining for decades. See the following table about the percentage of workers belonging to trade unions over time:

Except for the Nordic countries, where there was a meaningful decrease but current levels remain high, in most countries, workers’ participation levels are quite low. The relevance of collective wage bargaining in setting wages has logically followed the same decline. So, only some specifically skilled workers have the power to negotiate their wages, whereas the bulk are just dependent on general market conditions, forcing firms to adjust wages. All this is, of course, particularly clear in the US In a recent paper by Bloesch et al “ Do cost-of-living shocks pass through to wages? “ New York FED Staff Reports, n. 1126, October 2024, it is stated:

“We develop a novel, tractable New Keynesian model where firms post wages and workers search on the job, motivated by microeconomic evidence on wage setting. Because firms set wages to avoid costly turnover, the rate at which workers quit their jobs features prominently in the model’s wage Phillips curve, matching U.S. empirical evidence. We then examine the response of wages to cost-of-living shocks, i.e., shocks that raise the price of household’s consumption goods but do not affect the marginal product of labor. Such shocks pass through to wages only to the extent that higher cost of living improves workers’ outside options, such as competing jobs or unemployment, relative to their current job. However, higher cost of living lowers real wages at all jobs evenly, and unemployment is rarely a credible outside option. We conclude that wage posting and on-the-job search limit the scope for pass-through from prices to wages.“ … “In many advanced economies Union membership has declined dramatically, and evidence suggests that in the US wage-posting is the most common, if not dominant, method of wage determination” .

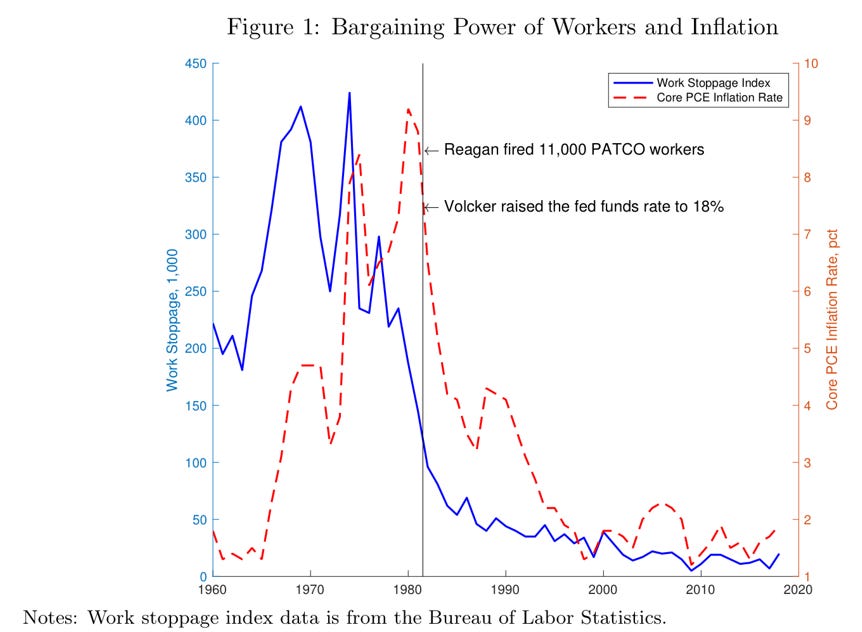

This type of development was visible everywhere during the previous inflation episode. The following figure from the same paper is a good illustration of the loss of workers pricing power since the 1960s and 1970s in the US:

All these points show that pure wage-price spirals are nowadays difficult to happen. Therefore, a) the price evolution expectations of consumers or households, it is not really very relevant as a cause of inflation, as their influence on wages and price decisions by firms is at best quite weak. Those expectations, obtained by surveys, are also problematic for two other reasons: b) it is easily documented that the perception of occurring inflation is usually grossly exaggerated upwards by households, and c) it is quite likely that their expectations are not a real anticipation of inflation but a simple extrapolation of observed inflation.

What is worrying is that central bankers are guided in assessing expectations by those type of household or consumers surveys . FED chairs have used the Michigan University Survey many times, and in her most recent speech, ECB Board member Isabel Schnabel used the ECB´s consumer survey [iii].

As I mentioned, the relevant inflation expectations are firms’ expectations. Unfortunately, in Europe, there are no good indicators of those. The only available source is a qualitative survey conducted by the EU Commission. In the US, there is only one good survey, initially coordinated by two well-known academics, Coibion and Gorodnichenko, which has later been conducted by the Cleveland FED. Regretfully, the respective time series starts only in 2018. The only two other direct sources of inflation expectations are those extracted i) from financial markets like inflation swaps or break-even inflation rates from bonds indexed to inflation, which have the problem that what is extracted is influenced not only by expectations but also by risk premia and market liquidity distortions; or b) from Consensus or the Surveys of Professional Forecasters, approximately two dozen of institutions/professional forecasters surveyed by the FED and the ECB.

In the ECB Working Paper Series No. 2604 (11 October 2021) “Do inflation expectations improve model-based inflation forecasts?”, using hundreds of variants combining several forecasting models and the four expectations sources, the conclusions are that all expectation measurements produce a modest improvement (maximum ≈ 10%), and that the best performers are the professional forecasters’ predictions. Those are not proper expectations but just forecasts made by economists who use the same types of methods that central bank staff use to produce their own forecasts. There is no proof that firms in general use such forecasts in their price decisions. The other result reported in the ECB paper is that incorporating expectations derived from financial market prices or those of firms and households does not lead to systematic improvements in forecast performance. A disappointing result which, while significant, has been ignored ever since. The final takeaway is that expectations as a cause of inflation have been quite exaggerated without further scrutiny. They have become one of those “established truths” that even other sciences disregard to scrutinise again during long periods of time. Michael Woodford’s monumental book of 2003 (Interest and Prices) has been able to impose the academic mantra that managing expectations is the crucial thing to do by Central Banks. Contrary to Phelps (1967) and Friedman (1968), who introduced expectations into the Phillips curve, modern theory with rational expectations is not concerned with questions about whose expectations are being considered or the real-life mechanisms through which expectations influence prices.

[ A parenthesis: Naturally, those using DSGE models with rational expectations don´t have to worry about secondary/tertiary matters, like whose expectations are considered or what the exact mechanisms are through which they influence price decisions. Rational expectations are precisely the method for endogenising expectations in the model, because they imply expectations that are compatible with, or, better, given by, the model itself. With a different model, expectations become different, but that is surely a detail. If one is using a small/medium-sized DSGE model without goodness-of-fit and forecasting efficiency tests, couldn´t we call the model-given expectations irrational for real-life decisions? [ii] Instead of calling the method as “consistent expectations” with the model, and naming it “rational expectations” was quite a rethorical coup, trying to make any alternative as irrational!.]

Coming price hikes in Europe?

All these considerations about second-round effects and expectations are topical because several European CBs appear to be preparing to hike rates in June. The CB of Norway did it a few days ago. The ECB Press Conference after the most recent policy decision meeting seemed to point to that scenario. It is, of course, data-dependent, meaning that if oil and gas prices increase further before that meeting as a result of possible US war escalation (to de-escalate down the road), some European CBs (not the FED) will actually hike rates in June.

One may suspect that the possible reasons for that will not be so much linked to the materialisation of second-round effects, but rather associated with a particular type of FOMO: the fear of missing out on rising rates without delay and of being accused of wrongly postponing them, as in 2021/2022. One ECB Board member said earlier that “ This time we will not wait”. This point deserves a further brief discussion.

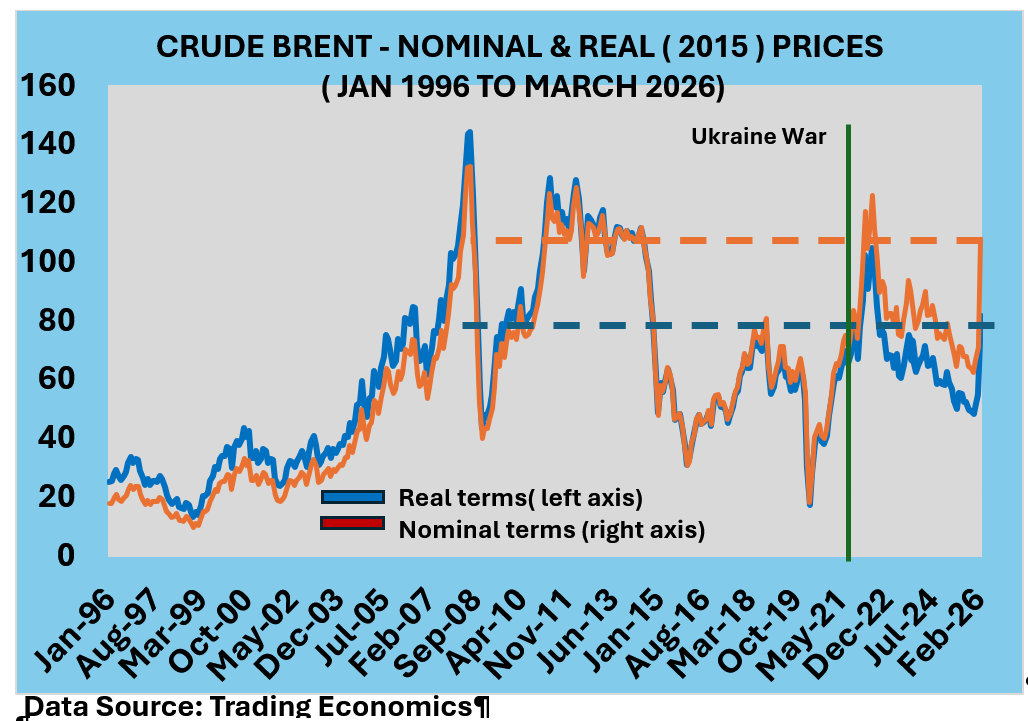

I think the postponing of interest rate increases was much more serious in the case of the FED than in the case of the ECB. The two inflationary processes were quite different, particularly in their initial stages, as in the US case there was the effect of a strongly expansionary fiscal policy that outpaced the Euro Area by several times. That explains the different inflation pattern shown in this table that starts in January 2021:

As you can see, in April 2021 inflation jumped in the US to 4.1, well above the Fed´s target, whereas in the EA it was only at 1.6. The difference stemmed from different demand pressures in the two economies. Inflation in the EA only surpassed 3% in September of that year, and it was the result of the normal recovery of oil prices after their abnormal low growth in 2020, when, in February, for a brief period, the oil price was below zero, and the average April price was $18.38. On the eve of the Russian invasion of Ukraine, the oil price was still equal to the 2018 level. It was then justified to think that, after such a recovery, oil prices would stabilise and that monetary policy could “see through” the supply shock and stay on hold. Then, on 24 February 2022, the Russian invasion of Ukraine triggered a totally unexpected jump in energy prices. This chart clearly shows that:

The FED reacted quickly and pivoted to a restrictive monetary policy in March 2022, while the ECB unexplainedly waited until July to do the same. That short delay by the ECB did not, in the end, compromise the success of both CBs in containing second-round effects by gradually increasing rates, helping to achieve a soft landing of the economy. At the same time, the usual waning of the international price shock brought down inflation. They correctly avoided “to do a Volcker” in a completely different situation of labour market institutions, as I explained in detail in my previous post here.

In my view, the ECB should not feel unduly constrained by giving in to pressure from “market literature” regarding the 2021/2022 episode. The ECB should, therefore, stay on hold for a while longer. That is what, for other reasons, the FED will do. After Kevin Warsh takes over, there will be no majority on the FOMC to lower rates or raise them, admitting that Warsh will not dare to defy Trump and propose a hike.

SUBSCRIBE FOR FREE TO GET ALL POSTS BY EMAIL

THE OTHER MISTAKE THE FED AND THE ECB MAY BE PREPARING

I refer to the possible demise of the type of floor system that both CBs are still pursuing (see my characterisation of both regimes here). Kevin Warsh wants to accelerate the shrinking of the FED balance sheet, abandoning a framework of “ample reserves” that is essential to the use of a floor system to manage the implementation of monetary policy. If he can achieve that, my prediction is that market liquidity turmoil will be such that he will be forced to backtrack.

Regarding the ECB, the issue is more subtle. The problem stems from the ambiguity contained in its 2024 Council decision about that implementation regime. A tension remains between those who interpret it as pointing to a soft form of a floor system, while others want to end up with a lean balance sheet without a structural portfolio and a small degree of excess bank reserves. A recent ECB Blog written by staff, while very useful in describing the new regime´s implementation so far, seems to point to the second interpretation, which, I believe, is a wrong interpretation of the Council decision. However, given the length of this post, I leave the subject for a future one.

[i] J. Goethe (1779), Der Zauberlehring, (The Sorcerer’s Apprentice), translated by Edwin Zeydel, 1955). The initial image of this post uses the painting with the same title by Margot Serowy.

[ii] Lars Svensson (1997) “Inflation Forecast Targeting: Implementing and Monitoring Inflation Targets,” European Economic Review 41 (1997), 1111-1146

[iii] See slide n. 6 of the speech by Isabel Schnabel (2026) “ The quite erosion of Central Banks independence” May 7th, 2026

[iv] This is the sort of mild provocation you can find in my preferred paper about expectations by Jeremy Rudd (2021) “ Why Do We Think That Inflation Expectations Matter for Inflation? FED Board Working Paper 2021-062

"Policy rate decisions

The task of Central Banks is always more difficult when the economy suffers a supply shock that has simultaneous effects: upwards on inflation and downwards on economic activity and unemployment."

All supply shocks (necessarily sectoral) have those simultaneous effects. But some supply shocks (COVID) are accompanied by negative aggregate demand shocks, too, so the downward side is redoubled.

The useful discussion of wage setting is in the end about how anchored are nominal expectations. How much danger is there of nominally downward sticky prices becoming real-ly downwardly sticky? Still, something to keep an eye on but not enough to prompt a preemptive tightening. I’d think TIPS data are useful although they could be more useful is Treasury woud create some intermediate 1.2. and 3year TIPS.

“The Fed reacted quickly and pivoted to a restrictive monetary policy in March 2022,”

Not quickly enough. TIPS expectations were above target by September 2021. The Fed was even talking about tightening in November. But that had to do with how quickly to disinflate after a supply shock response inflation, not about how much to inflate if any as a supply shock response.

I’d like to hear more about the fat/skinny balance sheet issue.

Well said on the inflation expectations issue.