FED CUTS, THE ECB HOLDS

Still, our economies are not controlled by Monetary Policy.

Predictably, the FED cut rates by 25 basis points to 3.50%-3.75% on December 10th, while the ECB remained on hold on December 18th, maintaining its policy rate at 3%. The FED lowered rates despite inflation being well above its 2% target, even after today’s unexpected headline figure of 2.7% for November, down from 3% in September.

Subscribe for free to get my posts by email

The main reason for doing that was to take insurance against the labour market weakness before it spirals out of control. As Powell stated at Jackson Hole in August, when he pivoted to announce cuts, “ … (the) situation suggests that downside risks to employment are rising. And if those risks materialise, they can do so quickly in the form of sharply higher layoffs and rising unemployment”. Layoffs have meanwhile occurred, as documented by the Challenger Survey, and the Unemployment Rate (U3) increased to 4.6% in November, the highest level since mid-2021. The more representative U6 unemployment rate, which includes those who want a job but have given up actively searching for it in the previous four weeks, and those who can only find a part-time job, was 8.3% in November, the highest since late 2021.

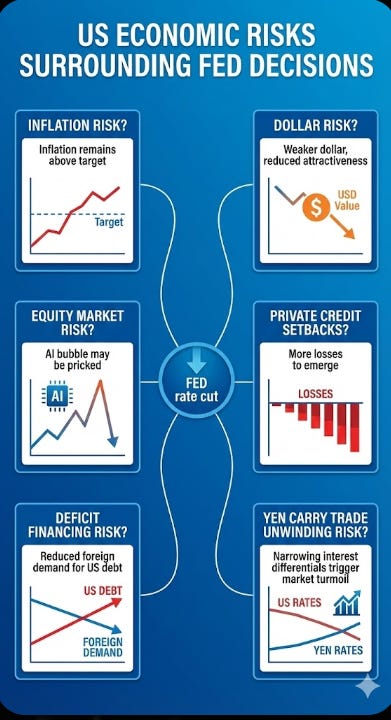

Financial markets responded positively to the rate cut, as indicated by their initial rise, reinforcing the view that another cut in January is now likely. However, there are two caveats: first, the November inflation figure, which shows a modest 0.2% increase since September and lacks October data due to the shutdown, may not be entirely reliable; second, markets remain wary of other factors that could influence asset valuations in the future. These include the possibility that inflation might persistently stay above target, the dollar could continue to slightly weaken, the AI bubble might burst, recent setbacks in Private Credit could quickly multiply, the US’s fiscally unsustainable situation could unsettle bond markets as foreign demand declines, and the increasing risk of an unwinding of the substantial yen-dollar carry trade could exert similar downward pressure. In future posts, I will unpack and evaluate these risks. A future FED, possibly under Trump’s control, will implement further cuts, but that will not suffice to address all these risks and could even worsen some of them.

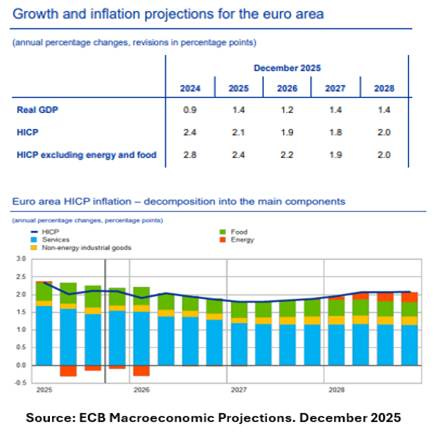

Economically, the short-term prospects for Europe seem more predictable, and the ECB kept its policy rate on hold at 2%, anticipating that it will continue “in a good place” reassured by its staff projections. Assuming tranquillity, i.e. no financial turmoil coming from the US, growth will go from 1.4% this year to 1.2% in 2026 due to the expected deceleration of world trade, only partially offset by good domestic demand growth, both consumption and investment. The projections are only about the Euro Area aggregates, but using other sources, what is foreseen for next year includes a jump in Germany’s growth from 0.3% this year to 1.1% in 2026. The 1.2% would be close to potential growth. From the perspective of forecasting ability, the long-term years of 2027 and 2028 would see a slight acceleration to 1.4%, based on an assumed recovery in world trade growth.

Inflation projections for 2026 have been revised upward from 1.7% in the September version to 1.9% now. This change is based on the stickiness of services inflation, which is now projected to increase by 3% next year, up from 2.7% in the September forecast. Services inflation, in turn, is related to different wage growth projections: 2.2% in September and 2.6% now. For 2027 and 2028, inflation is expected to remain well-behaved at 1.8% and 2.0%, respectively. If such a baseline forecast were to materialise, the ECB could easily stay on hold throughout the entire period… Can anyone believe that? In a recent Bloomberg survey, a robust majority of specialised economists believe that until the end of 2027, although two minorities predict either a hike (a bigger tail) or a cut (a smaller tail) long before then.

The Bloomberg article stated that

“More than 60% of respondents in a Bloomberg survey say officials are more likely to raise borrowing costs than lower them — a meaningful change from October, when only a third shared that outlook.

It’s not something they expect to happen anytime soon, however: The deposit rate is seen remaining at 2% on Dec. 18 and throughout the next two years.”

The first sentence sensationalises the idea that the next move is upward, but the second sentence reassures by correctly stating that economists do not predict this over the next two years at least. Somehow, only the first sentence resonated, adding some spice to an otherwise mostly predictable and dull ECB meeting. That was because of the following extract from the Bloomberg interview with the ECB Board member Isabel Schnabel (Questions are in bold, answers in normal font):

“ The very obvious next question then is: where are we in the policy cycle? Has the rate-cutting cycle come to an end?

Interest rates are in a good place, and in the absence of larger shocks, I expect them to stay in this place for some time. The distribution of inflation risks has shifted to the upside, and accordingly, both markets and survey participants expect that the next rate move is going to be a hike, albeit not anytime soon.

……

So do the expectations for the next move to be a hike feel right? Would you agree with those expectations?

I’m rather comfortable with those expectations.

Some economists have pencilled in a first hike for June 2026. A majority sees it by the end of next year. Does that sound reasonable?

At this point in time, this remains very uncertain. This is not currently on our minds. We’ll cross that bridge when we come to it.”

A distant possible event was then spuriously animating the ECB Press Conference as if it were something imminent.

Closing this parenthesis, what stems from the projections and the meeting is a possible uneventful period ahead for the ECB. Forecasts cannot, of course, account for event uncertainty and many things can happen in the world in the near future.

Nevertheless, what all these underscores is that Europe’s main problems are of a deeper nature. They are structural (low potential growth), political (internal dysfunctional fragmentation), and geopolitical (bullied by a new adversarial America, attacked by Russia, and economically threatened by China). In the new Trump world, there is no room for complacency or naive optimism. I will address those deeper problems in future posts.