CENTRAL BANKS BRIEFLY IN "A GOOD PLACE" - SINTRA’s ECB FORUM

Central Banks enjoyed a brief moment of being in “a good place”, which will be changed soon by weaker economies, trade shocks and even…stablecoins

The ECB Monetary Forum in Sintra took place this week and hosted the usual successful gathering of academics and policymakers, along with the customary networking and corridor gossip. European hopes of renewal were running high, mixed with an anguished fear that Governments will fail again to make the bold decisions needed to seize the moment.

The meeting's success was ultimately assured, despite starting with two disappointing research papers. The first, on “ Eurosclerosis at 40: Labor Market Institutions Dynamism, and European Competitiveness”, aimed to demonstrate that persistent rigidity in the labour market is the cause of the innovation gap between Europe and the US. The paper is valuable in illustrating that, following the 1980s debate on the sclerotic European labour market being responsible for high unemployment at the time, the issue was effectively addressed through significant reforms such as expanded fixed-term contracts, part-time jobs, and the diminishing role of trade unions and collective bargaining.

Recognising the acquired flexibility, although at the expense of some duality in the labour market, the paper introduces a so-called “new view” that the labour market's lack of dynamism is responsible for the absence of innovation, as workers are hesitant to switch to new jobs being offered, making innovative investments riskier and less likely to be undertaken. The evidence for this causal link is weak, and the alternative view — that the main reason Europe missed out on the ICT revolution in the 1990s — is more convincing. Indeed, if we examine the US experience, we see that the emergence of the current big tech firms was driven by vigorous venture capital activity, which can only exist because of a deep and liquid capital market where IPOs of successful companies more than compensate for all the venture capital losses. This is also supported by European innovative firms that move to the US in search of capital and financing, while most of their workforce remains in Europe.

The second paper is surprising because it relies on a stylised early version of DSGE models with a representative agent, which is used to justify the idea that the business cycle is driven by discretionary consumption expenditures, excluding expenditures on necessities and investment in housing or firms. I was fortunate to attend the 2007 FED Jackson Hole meeting, where the highly respected Edward Leamer, who sadly recently passed away, presented his well-known paper “Housing is the business cycle”, offering a much more convincing case, especially for the US. In the model presented at Sintra, there is no fixed investment, similar to the models before the Smets-Wouters paper. GDP consists solely of consumption in a closed economy. Among consumption, discretionary spending could sufficiently explain the economic cycle, whereas the consumption of necessities would account for aggregate inflation. The authors even suggest that monetary policy should target inflation in the necessity consumption segment, as this would be the optimal policy in their stylised closed economy model. This contrasts with focusing on core PCE inflation as the FED does, and it hardly warrants further consideration.

After the first two research papers, the Forum continued with two insightful panels—one discussing the implications of heterogeneity among member countries for monetary union, and the second featuring monetary policy discussions with Central Bank Governors or Presidents from the UK, South Korea, the US, the Euro Area, and Japan. The first panel was particularly engaging, and I would like to highlight the interventions of Luca Fornaro and Refet Gürkaynak. Luca addressed the potential stagnation effects of poor fiscal policy, concluding with a slide summarising his findings.

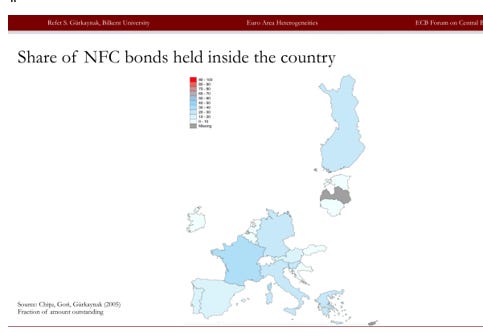

Refet underlined the surprising fact that the corporate bond market does not show much heterogeneity as most of issued bonds were placed over all countries of the area, as the placement was not biased towards domestic investors. This slide illustrates the conclusion:

However, it must be emphasised that the corporate bond market in Europe is quite small, amounting to 1.7 trillion compared to the US market with 11.5 trillion. This implies that the European market is predominantly accessed by large firms, which find demand more easily in most European countries.

The FED and the ECB are enjoying a brief period of being in a “good place”, but will soon face new challenges, from a deteriorating economy, trade shocks and even … stablecoins

The CBs policy panel aligned with their well-known official positions. The only novelty came from Jay Powell when he did not explicitly exclude July from a possible discussion of a rate cut, without, of course, affecting the likelihood of maintaining current rates, which is what everyone expects. He also reaffirmed that the FED will honour its commitment to the swap lines already negotiated with other CBs, which was seen as a novelty by some media despite not being the case, as he has expressed the same in public statements, particularly in a recent interview or conversation with Raguram Rajan.

The US economy is clearly slowing down, and this trend is expected to persist throughout the year. The final revision of Q1 growth now shows a contraction of – 0.5%, revised downward from the previous estimate of 0.2% due to a decrease in consumption. Personal income fell by -0.4% in May, accompanied by a decline of -0.1% in personal spending. Exports in May dropped by -5.2% compared to April. Housing sales were down year-on-year by -0.7% in May, and the ISM Manufacturing New Orders subindex decreased to 46.40 points in June 2025 from 47.60 in May. In June, the US has three different sources of jobs/employment figures: the BLS Households survey (a sample of 60000); the BLS Payroll Survey (focusing on job positions, not number of workers employed, with a sample of 119000 employers), which indicated +147000 positions in June; and the ADP (covering employees in private firms only, with 25000 workers), reporting that firms reduced the workforce for the first time in two years, with a decrease of 33,000 instead of an expected increase of 100,000. Finally, so far this year, US firms have announced 744300 job cuts (including Microsoft’s 4% reduction of its US workforce), the highest figure for this period since 2020. These and other indicators suggest a potentially weak second quarter, and by autumn, the FED might need to cut rates, assuming end-game tariffs do not cause significant price rises, whether their impact is “one-off” or “temporary”. Rate cuts are expected to occur in the Autumn, but the pressure to cut rates earlier, driven by Trump, will be relentless.

The ECB will face challenges after the summer, with a weak economy and quite low inflation. By the autumn, inflation could reach 1.5% and economic growth just below 0.5%. These outcomes remain conditional on “reasonable” US tariffs, but are driven by their negative growth impact, the continued decline in oil prices, ongoing euro appreciation, and a decline in wage increases, as indicated by the ECB's wage tracker at 1.6% for the fourth quarter.

The new Strategic Framework that the ECB announced on Monday, the first day of the Forum, doesn’t differ significantly from the one introduced in 2021 and doesn't preclude the pressure for further cuts in such a scenario. Nevertheless, the new Framework deserves a more detailed discussion, which I will provide in a future post.

Stablecoins and … Central Bank Digital Currencies (CBDC)

Another disruptive force will soon emerge from the surge of dollar-linked stablecoins entering the global payments market, leading to significant consequences across various sectors. Many firms in Europe will start to adopt them, challenging the insufficient regulations in the EU and possibly impacting Central Bank Digital Currency projects. A key point in the Governors' Panel was the confirmation that the ECB was the only participant continuing to prepare a CBDC initiative. Among major Central Banks, we may end up with the ECB and the People´s Bank of China issuing CBDCs.

The South Korea CB Governor revealed that, despite completing their preparations to launch their own digital currency, they decided to halt the project. One reason he mentioned was the imminent spread of dollar stablecoins following the US Senate's approval of related legislation. Europe needs to amend MICA, its own regulation that addresses this matter, and the ECB must seriously consider the issue. The Bank of England Governor, Andrew Bailey, stated in a recent speech that he is not convinced about the merits of a CBDC. In November, the BoE published an official position on the regulation and support for stablecoins. The British Parliament expanded the Bank of England's powers to regulate stablecoins, and the 2023 official document states that “Stablecoins issued outside the UK will need to be approved for use in payment chains within the UK”. European Union authorities have taken no recent action regarding this matter. The issue is complex, and I will dedicate a lengthy post to explaining my views on what should be done.

The research papers on the second day of the Forum were better.

Considering the length of this Post, I can only briefly comment on the two research papers presented on the second day of the event. The first one was on “ Non-Bank financial intermediaries, liquidity and their prudential treatment” and highlighted that the size of the sector has surpassed banks´ assets, with which NBFI are more intertwined via funding flows. Therefore, NBFIs exert a large influence on financial conditions that are the transmission channel of monetary policy. The difficult and controversial discussion about possible access of NBFIs to Central Bank liquidity is also addressed with better caution than the one displayed by the IMF in its April 2023 Global Financial Stability Report. The paper showed how the asset side of the growing NBFIs displays a very sizable portfolio of foreign assets, funded, of course, by European savings. What the paper presents as a fact is often regretted in policy Reports and EU Commission texts, and used as a justification for the so-called Savings and Investment Union to avoid the export of capital. In a comment from the audience, I reminded the authors that the question has a fundamental macroeconomic dimension. The macroeconomic regime applied in Europe, under the influence of Germany, does not rely sufficiently on domestic demand and aims for an External Current Account surplus, seen as an indicator of economic success. By definition, an economy that has a Current Account surplus is an exporter of capital, as the Balance of Payments, including the variation of official external reserves, adds to zero. The reduction of applying capital abroad depends ultimately on changing the growth regime adopted in Europe.

The second paper had the title “ New industrial developments and the evolving architecture of international trade”. Naturally, it was focused on the changes introduced by the entrance of China into the world economy. and a very rich content of data analysis. It is also very rich in broad data analysis, and a number of specific indicators that it uses. A few slides provide a hint about what I am referring to:

This slide illustrates how China's composition of exports in high tech and patents has become quite similar to the EU's, proving both are competing in the same tech sectors where China is growingly penetrating the European market.

The next slide shows that, strategically, the US began to decouple from China imports some time ago, whereas Europe has increased its dependence on China imports since 2017.

I hope these two slides entice you to read the more useful paper presented at the ECB´s Sintra Forum.

Many thanks! - What a wonderful summary of Sintra.

I was - again - struck by the ECB’s lonely stance on CBDC. I continue to see it as solution looking for a problem, although dependence on a unreliable US may now be “that problem” (ie a European retail payment system would be “the solution” spinning off the digital euro - although a payment system really shouldn’t be inside a central bank).

I look forward to your thoughts on stable-coins. Today’s FT Alphaville has a detailed “hold your horses” assessment. Lorenzo Bini-Smaghi has a more optimistic view in his FT column, in which he calls for European leadership and action.